Prescription drugs, jackball.

If you haven’t done your national duty and signed up for government-mandated health care, a) get back in line, prole but 2) read this first. You can game the system for hundreds of dollars.

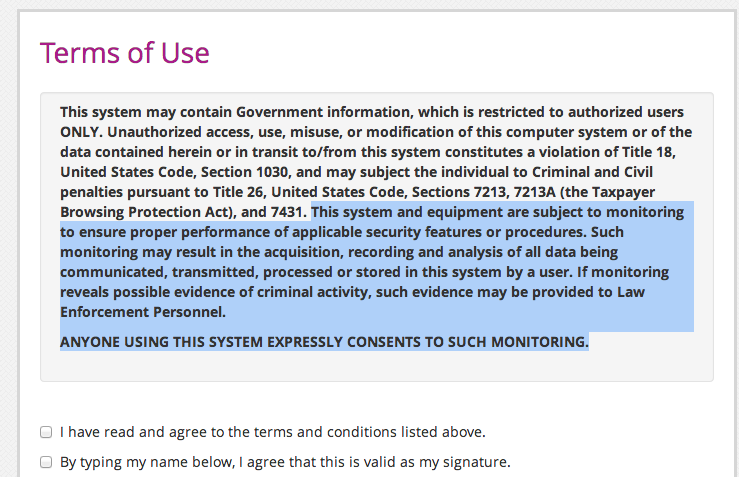

We’re not going to discuss the inherent instability of ObamaCare, nor how it was designed to fail so it could be the first step to the inevitability of pure socialized medicine. Hell, you people are the ones who voted for it, not us. Nor are we going to explain how cumbersome, inconsistent, sclerotic and self-contradictory the process of submitting to your bettors and purchasing government-approved insurance is. We already did that, and it hasn’t gotten any better. Click on the link, but we’ll repeat the most ominous line from the ObamaCare user agreement here:

This system and equipment are subject to monitoring to ensure proper performance of applicable security features or procedures. Such monitoring may result in the acquisition, recording and analysis of all data being communicated, transmitted, processed or stored in this system by a user. If monitoring reveals possible evidence of criminal activity, such evidence may be provided to Law Enforcement Personnel.

ANYONE USING THIS SYSTEM EXPRESSLY CONSENTS TO SUCH MONITORING.

Caps in the original.

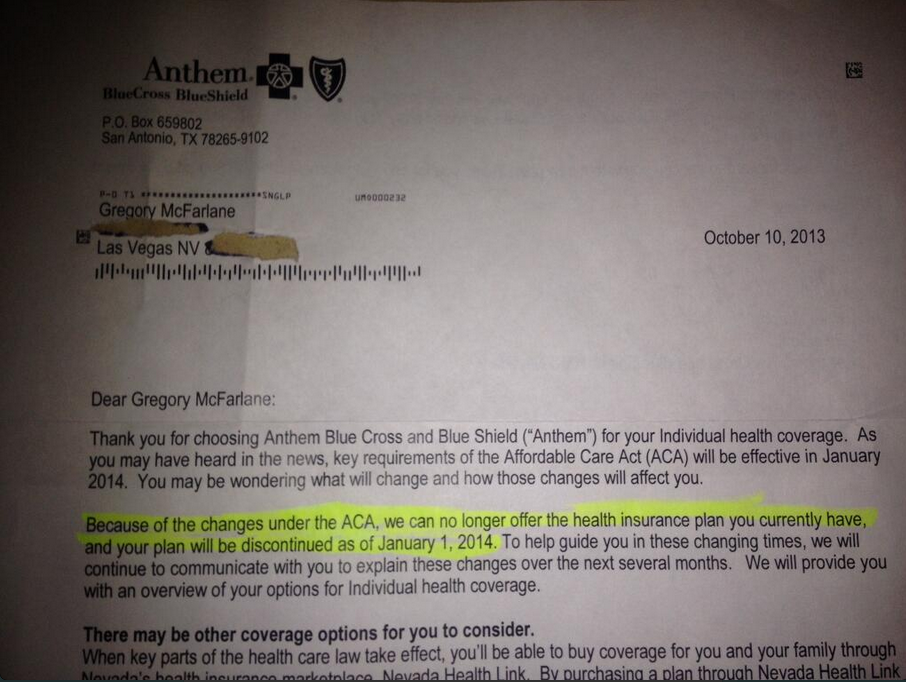

Our state, Nevada, has given most-favored-insurer status to Culinary Workers Union Local 226, the local Marxists and the creators of the state health exchange. Unions still wield considerable power in the Sagebrush State, due to it having high demand for workers who shut up and do what they’re told without any actual skills getting in the way (coffee servers, roulette dealers, etc.)

So, a young and fit Control Your Cash principal with a grand total of zero major and one minor health problems (easily controlled hypertension) avoided the fine and bought hisself a policy. On the surface, the math doesn’t seem to work out:

The policy is $311 a month, with an obscene $6250 annual deductible. A free market being the last thing you’d want in the purchase and sale of health insurance, that was the least bad policy among the 11 offered. Every last one of those policies includes maternity coverage, despite its sole insured being a) male, 2) pedophobic and iii) permanently sterile. Still, you never know when a guy might wake up one morning and find himself with functioning and fertile ovaries.

(Aside: The user-unfriendliness of the state exchange sites is a given, but what we found especially vexing was what the creators assume about the users’ knowledge. Our own state’s site includes the Frequently Asked Question “What is insurance?”, implying that they’re writing this for the lowest common passably literate denominator. Okay, fine. But the very same site then offers “gold”, “silver” and “bronze” plans, introducing new terms without explaining what the differences among them are. Your only hope is to open a few dozen browser windows and compare one plan to another line-by-line. Our state also offers “catastrophic” beside the precious metal descriptors; we incorrectly assumed that such a policy would cover only, you know, catastrophes. Like broken legs and ruptured spleens. But no, it’s as comprehensive as the platinum plans.)

It’d seem to make more sense to suck it up and pay the $95 fine to the IRS, rather than commit to between $3732 and $6250 in medical spending over the next year. (Because it’s the Affordable Care Act, remember?) One problem, however. The drugs.

The hypertension is controlled with a gift from the greatest corporation on Earth, Novartis. They make a pharmaceutical that completely eradicates the insufferable, debilitating headaches that used to show up regularly and portended a stroke. As far as we’re concerned, the $9 billion Novartis made last year wasn’t nearly as much as they deserved. But such a wonder drug ain’t cheap. Ten bucks a day.

You can either whine about governmental incompetence, or you can use it to your advantage. Drug retailer Walgreens issued a press release on December 30 (a/k/a “United States citizens’ penultimate day of health care freedom) that preempted or at least postponed the deluge:

The release was written by a public relations hack, which means it’s 20 times longer than it needs to be, so here’s its only relevant sentence:

Through the end of January, patients can bring confirmation of their enrollment in the public health insurance marketplace to a Walgreens pharmacy, or the pharmacy staff can check to verify eligibility, and Walgreens will assist them by providing up to a month of a traditional, brand and generic medication (sic) at no upfront cost.

We tried this, and it freaking worked. Did we mention that the public health insurance marketplace in question might not even demand your first payment for a month or two? Buy a policy now, in any state, and chances are good that it won’t even activate until March 1 or April 1. And again, you don’t have to pay then and there. But getting fronted $311 worth of drugs (or more, your prescriptions may vary) from either an awfully trusting or awfully connected drugstore chain happened just like that.

What’s to stop us from cancelling our policy, especially given that we haven’t even filed any claims yet, and pocketing the hypertension drugs? Unclear. Don’t think we haven’t thought about doing this again by the January 31 deadline. And it’s not as if Walgreens can somehow get its (S)-3-methyl-2-(N-{[2′-(2H-1,2,3,4-tetrazol-5-yl)biphenyl-4-yl]methyl}pentanamido)butanoic acid back once it’s been consumed with coffee and a bagel.

Is this unethical? Sorry, counselor, we reject the premise of the question. The rules have changed. Buying too much house and having it fall into foreclosure is now “being preyed upon by unscrupulous lenders.” Violating immigration law is now “Ningún ser humano es ilegal.” Gaming the healthcare system? Sorry, that’s the American way. As we once heard from a septuagenarian man who crossed into traffic and destroyed our vehicle, trying to appease us before the tow truck arrived and/or he became our garroting victim, “Let’s just let the insurance companies sort it out, huh?”